Insights into IAS 36

INTERNATIONAL FINANCIAL REPORTING STANDARDSInsights into IAS 36 provides assistance for preparers of financial statements and help where confusion has been seen in practice.

For entities that operate in a variety of classes of business, geographical locations, regulatory or economic environments or markets, high quality management accounts are essential. They enable management to monitor performance, allocate resources and devise business and market strategies. IFRS 8 ‘Operating Segments’ requires much of this management information for public listed entities to be published externally so that investors, analysts and other users of entities’ financial statements can review an entity’s operations from the same perspective as management.

The objective of IFRS 8 is set out in a core principle. This principle requires an entity to disclose information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates.

Operating segments are determined based on the structure of the organisation and how information is reported to management. IFRS 8 does not prescribe the measurement policies for the information to be disclosed. Instead the amounts disclosed are mainly based on the information presented to management. This is generally known as ‘the management approach’ or ‘through the eyes of management’.

The management approach

The IASB decided to implement a management approach in the Standard because:

IFRS 8 requires an entity to disclose information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates.

IFRS 8 requires an entity to report financial and descriptive information about its reportable segments

IFRS 8 specifies how an entity should report information about its operating segments in annual financial statements and, as a consequential amendment to IAS 34 ‘Interim Financial Reporting’, requires an entity to report selected information about its operating segments in interim financial reports.

Generally, financial information is required to be reported on the same basis as is used internally for evaluating operating segment performance and deciding how to allocate resources to operating segments. IFRS 8 requires reconciliations of total reportable segment revenues, total profit or loss, total assets, liabilities and other amounts disclosed for reportable segments to corresponding amounts in the entity’s financial statements.

IFRS 8 sets out requirements for related entity-wide disclosures about products and services, geographical areas and major customers. It also requires an entity to report information about the revenues derived from its products or services (or groups of similar products and services), about the countries in which it earns revenues and holds non-current assets, and about major customers, regardless of whether that information is used by management in making operating decisions.

IFRS 8 does not require an entity to report information that is not prepared for internal use if the necessary information is not available and the cost to develop it would be excessive.

If an entity changes the structure of its internal organisation that results in a change in its reportable segments, then the corresponding amounts should be restated unless, for each item of disclosure, the information is unavailable or the cost to develop it is excessive. Where comparative information has been restated, this fact should be disclosed.

The disclosure requirements of IFRS 8 are limited to entities within its scope. However, other entities may, in certain circumstances, need to identify operating segments in accordance with IFRS 8 in order to comply with the requirements of other standards (see more details below).

Identifying entities within the scope of IFRS 8

IFRS 8 applies to entities that prepare financial statements, and:

This applies to both consolidated financial statements of a group with a parent and the separate or individual financial statements of an entity.

IFRS 8 clarifies what is meant by a ‘public’ market and makes it clear this includes ‘over-the-counter’ markets. It also states a parent entity that does not have publicly traded securities is not within the scope of IFRS 8, even if it has a subsidiary or investment in another entity that has issued listed securities.

If a financial report in the scope of IFRS 8 contains both consolidated financial statements as well as the parent’s separate financial statements, segment information is required only in the consolidated financial statements.

Some entities outside the mandatory scope of IFRS 8 may decide to disclose segment information regardless. If this happens but the entity chooses to disclose information about segments that does not comply fully with IFRS 8, it must not describe the information as segment information. An alternative heading should be given to the disclosures.

Implications for all entities, including those outside the scope of IFRS 8

Although entities outside the scope of IFRS 8 are not subject to its disclosure requirements, they must still use the guidance to identify operating segments when identifying cash generating units (CGUs) or groups of CGUs to which goodwill or mineral resource exploration and evaluation assets are allocated.

A number of other standards refer to segment information or the identification of segments in accordance with IFRS 8. In some circumstances, additional disclosures relating to segments are only required for entities within the scope of IFRS 8. However, in some situations, the requirements of other standards relating to segments apply to all entities, including those outside the scope of IFRS 8.

In a later article we will discuss the interaction of other standards with IFRS 8 and we will highlight additional requirements of other IFRS for entities that fall within the scope of IFRS 8.

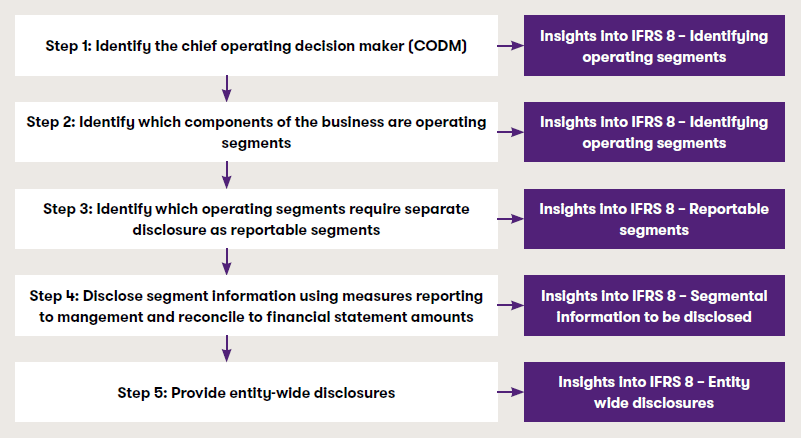

The process for determining operating segments and identifying which of those are reportable separately is summarised in the flow chart below.

How to address each of these five steps will be explained in subsequent articles in the 'Insights to IFRS 8' series.

We hope you find the information in this article helpful in giving you some insight into IFRS 8. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact or contact your local member firm.

Insights into IAS 36 provides assistance for preparers of financial statements and help where confusion has been seen in practice.