As the final text of the ESRS is now available, companies within their scope need to get ready now as some reporting entities within the scope of CSRD will have to apply ESRS for reporting periods commencing on or after 1 January 2024.

The following FAQs will help you understand a bit more about the CSRD and the ESRS that have been released.

What is the CSRD?

On 5 January 2023, the Corporate Sustainability Reporting Directive (CSRD) entered into force. It builds upon its predecessor the Non-Financial Reporting Directive (NFRD), which was issued in 2018. The CSRD expands the scope of entities who will have to disclose sustainability information, and introduces requirements (particularly across basis for preparation, strategy and business model, due diligence, governance, risk and opportunity management, and targets and metrics) that are more detailed. In addition, there are more detailed disclosures under Environmental (E), Social (S) and Governance (G) topics, collectively known as ESG.

The NFRD applied to large and listed entities which totalled approximately 11,000 EU entities. The CSRD is estimated to apply to circa 50,000 EU entities. Entities in scope will have to include disclosures as part of their annual management report alongside their financial statements and for the same reporting periods. This reporting will cover both the entity’s own operations and its value chain.

What is the objective of the CSRD?

The objective of the CSRD is to improve the existing requirements of the EU’s Non-Financial Reporting Directive (NFRD), to better harness the potential of the European Union in the transition to a fully sustainable and inclusive economic and financial system, in accordance with the European Green Deal and the UN Sustainable Development Goals.

The new rules will ensure that investors and other stakeholders have access to the information they need to assess investment risks arising from climate change and other sustainability issues. They will also create a culture of transparency about the impact of entities on people and the environment.

What is the timeline for CSRD?

The CSRD forms part of the European Union’s Sustainable Finance package of regulations including Sustainable Finance Disclosure Regulation (SFDR) and EU Taxonomy. The first set of standards were delivered to the EU Commission by EFRAG (European Financial Reporting Advisory Group) in November 2022 with the final text of the CSRD issued on 6 December 2022.

Which entities will be in scope for CSRD?

The CSRD will apply to circa 50,000 entities on a staggered basis for fiscal years beginning on or after 1 January 2024. This will initially apply to those already reporting under NFRD for the financial year 2024, so reporting in 2025. Other entities meeting the scoping criteria as set out in CSRD will need to report from FY 2025 onwards with SMEs and EU subsidiaries coming into scope later and up to FY 2028.

The scoping criteria confirms the CSRD applies to all entities, including subsidiaries of non-EU parents, that have debt or equity securities listed on an EU-regulated market (other than micro-entities). Additionally, the CSRD also applies to all EU entities that meet at least two of the following three criteria on its two most recent consecutive balance-sheet dates:

- Total assets exceeding €20 million

- Net turnover exceeding €40 million

- 250+ employees.

Additional rules and scoping criteria apply for Group and EU Subsidiary entities of non-EU parents as defined within the CSRD.

Consolidated sustainability reporting also applies to sustainability statements and goes beyond consolidation requirements covered within the financial statements with entities needing to provide an adequate understanding of the risk / impacts of the subsidiaries across any material topics.

What is the difference between NFRD and CSRD?

NFRD brought very large and listed entities into scope for sustainability reporting. CSRD broadens the scope in terms of entities required to prepare sustainability statements. Under CSRD, entities must assess their eligibility against three criteria including average number of employees (>250), total assets (>€20m) and turnover levels (>€40m). EU entities meeting two of the three criteria set out will be in scope for CSRD. Additional scoping and consolidation considerations for non-EU entities and their subsidiaries also need to be considered.

The most significant difference is the introduction of mandatory reporting standards under the CSRD in the form of the European Sustainability Reporting Standards (ESRS). Entities reporting under CSRD must apply these EU sustainability reporting standards and bring sustainability information into their annual management report, applying the same reporting period for both.

Which ESRS will apply to the first entities reporting under CSRD?

The EU Commission is at the final stages of approval of the first tranche or Set 1 of the ESRS (includes two cross cutting and ten topical standards across E, S and G). The last public consultation on the final amendments closed on 7 July 2023 and the final text was issued within the EU Delegated Acts on July 31 2023.[i]

The draft ESRS take into consideration existing EU regulation such as the SFDR and Taxonomy regulations, as well as considering international initiatives such as the ISSB, TCFD and GRI, in order to try and lessen the burden on entities by avoiding duplication of disclosures. EFRAG has issued a number of reconciliation and navigation tables within the Appendices to the draft ESRS (Refer to Appendices 1 to 6) linking disclosures within ESRS to other relevant regulatory reporting frameworks.[ii]

What topics are included in the first set of ESRS?

The first set of ESRS includes two 'cross cutting' and ten topical standards across the three ESG areas.

- ESRS 1 is the conceptual framework of ESRS and does not contain any specific disclosures but is guidance in the application of ESRS for entities in scope, and includes explanations and guidance around double materiality, value chain disclosure and sustainability due diligence. In addition, it includes examples on presentation, structure of sustainability statements and guidance for draft transitional provisions upon first time adoption.

- ESRS 2 General Disclosures is mandatory for all entities in scope for CSRD. ESRS 2 includes disclosures required around basis of preparation, governance structures and due diligence procedures, strategy and business models and impacts, risks and opportunity management for entities. It is expected that all topical standards will be subject to a double materiality assessment by entities, in order to determine what should be disclosed.

Note - As part of the EU public consultation, ESRS E1 ‘Climate’ and ESRS S1 ‘Own Workforce’ (1-9) were amended. The EU Commission proposed that these Standards, alongside the rest of the topical ESRS, are subject to a double materiality assessment, which has now been approved. ESRS 2 is the only standard that is now mandatory and not subject to the double materiality assessment process. - ESRS E1 to E5 related to topical Environmental disclosures, ESRS S1 to S4 related to topical social disclosures and ESRS G1 relates to topical governance disclosures as outlined below.

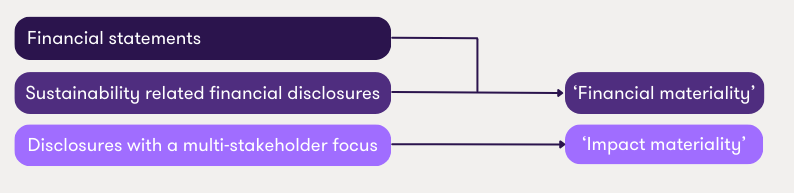

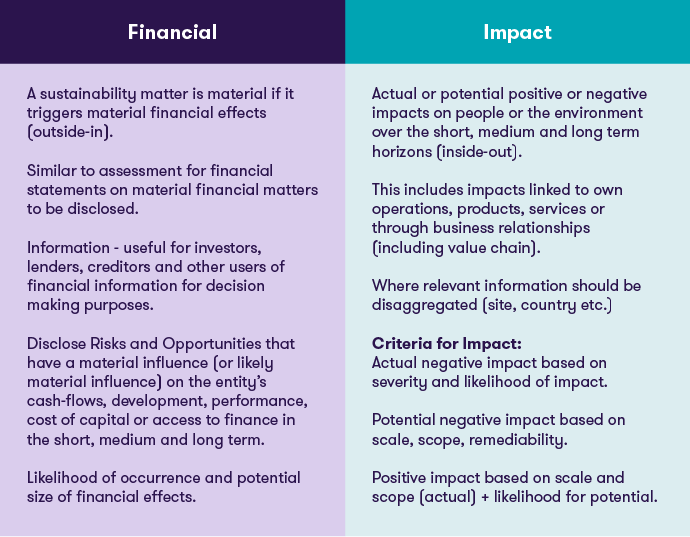

What is the 'double materiality' principle?

The CSRD and ESRS introduce the concept of double materiality. Entities applying ESRS must report material impacts, risks and opportunities or 'IROs' across each topical area within their sustainability statements that are both financially impactful (outside in) and have an impact to people and the environment (inside out).

These disclosures will cover both the entity’s own operations and its upstream and downstream value chain. However, the ESRS contain some transitional reliefs in respect of the value chain. Implementation guidance on both the Materiality Assessment process and Value Chain provisions are currently in draft and will be issued by EFRAG in Q4 2023. Current drafts of this guidance are available for review but currently are subject to change and final approvals.[iii]

Double materiality concept: Summary overview and concepts

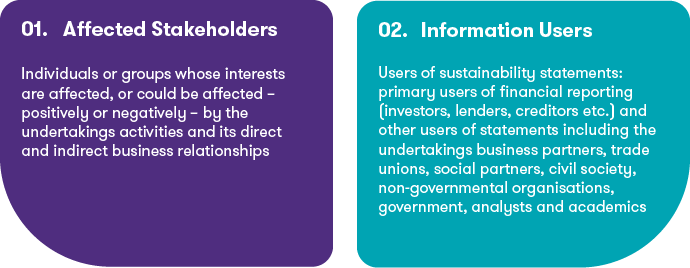

Stakeholders and their relevance to the materiality assessment process

Within ESRS, stakeholders are defined as both users of sustainability statements and other stakeholders or information users. Stakeholders are those who can affect, or be affected by, the organisation and both need to be incorporated into the due diligence process.

What phase-in reliefs have been provided?

The European Financial Reporting Advisory Group (EFRAG) and then subsequently the European Commission, through its final consultation process, have provided some phased-In Disclosure Requirements that will help reporting entities, particularly smaller entities that would be subject to sustainability reporting requirements for the first time.

The full list of phased-in requirements is included in ESRS 1: Appendix C

| Year 1 | Year 2 | Year 3 |

|---|---|---|

|

Comparative information is not required

|

||

|

Datapoints related to their own workforce in ESRS S1 – social protection, persons with disabilities, work-related ill-health, and work-life balance are not required

|

||

|

Financial effects related to non-climate environmental issues (pollution, water, biodiversity, and resource use) are not required, qualitative disclosures can be provided in the first three years.

|

||

|

In the absence of sector-specific standards, other available frameworks could be used to develop specific disclosures if required for material entity-specific sustainability matters not included in the first set of ESRS.

|

||

|

Company-specific disclosures that were developed prior to the ESRS being adopted can still be used.

|

||

|

There is a requirement to consider value chain as part of materiality assessment process but data gathering aspects are limited for the first three years and information on the value chain can estimated or omitted if the information is not available during this time.

|

||

A summary of phased-in Disclosure Requirements for all reporting entities is outlined below:

| Year 1 | Year 2 | Year 3 |

|---|---|---|

|

Scope 3 Greenhouse Gas (GHG) emissions data, and ESRS S1 disclosures are not required.

|

||

|

The disclosure requirements for biodiversity (ESRS E4), Workers in the value chain (ESRS S2), Affected Communities (ESRS S3) and Consumers and End-users (ESRS E4) are not required.

|

||

In addition, until 2030, EU subsidiaries of non-EU parents can prepare just one report, which includes subsidiaries that would ordinarily be required to report separately, due to size or if they are listed.

What's a reporting boundary and what needs to be considered?

CSRD expands the reporting boundary for undertakings beyond their own operations to include both upstream and downstream value chain activities. An undertaking must report material impacts, risks and opportunities within the value chain against ESRS disclosures or if other material impacts exist not covered by ESRS include entity specific disclosures. This applies to all tiers of the value chain.

Where value chain information is not available, entities can use internal or estimated data or sector proxies during the initial transitionary periods. The ESRS contain phasing-in reliefs in the first three years of implementation if this information is not available. Refer to phasing-in FAQ for more information.

Am I ready for CSRD implementation?

Depending on when you come into scope for CSRD and what your maturity level is with respect to your sustainability strategy, structures and reporting process, you may have a number of areas to consider including:

We can help

We hope you find the information in this article helpful in beginning to understand the requirements of the CSRD. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact or your local member firm.