The people of the United States have voted and the new US President is Donald Trump. While it’s still too early to tell the final outcomes we outline some of the global expectations and implications of this result.

Headlines

- The next US President will be Donald Trump.

- The republicans will retain control of the Senate and House of Representatives.

- The new administration will take a different approach to trade agreements, however, the future official position is unclear which contributes to short term trade related volatility. Uncertainty tends to dampen both inward foreign and domestic outward investment potentially weakening the dollar which could provide a boost to US exports.

- Longer term, the prospect of protectionist policies from the US may impact exporters to the US and invite retaliatory action against US exports, but could also open the way for governments to seek trading relationships with the US.

Understanding Congress

The legislative branch of the US Government is the Congress and is made of two parts: the US Senate and the US House of Representatives. Each state has two US Senators and at least one US Representative; the more residents a state has, the more US Representatives it is allowed. There are 100 US Senators and 435 US Representatives.

The US’s complicated system makes election night a race to secure a majority from the 538 votes in the electoral college, a body of people who represent the states of the US.

The big question beyond the presidency is what will happen in the Republican-controlled Congress. Mr Trump has not hitherto enjoyed absolute support of his Republican party, and it remains to be seen whether his big policies will survive Congress or be diluted or even shelved.

The campaign has been divisive and at times filled with bitter criticism and malice between the candidates. It seems clear that the winners and losers will continue to argue long after the declared election result.

Predicted scenarios

The impacts of the election are sure to be far and wide. We outline some of the influence on politics; trade; markets; and interest rates:

Impact of Congress:

- Mr Trump has not always enjoyed the undiluted support of the Republican party – it is at least possible that Republicans in the House especially do not support Mr Trump or his policies, leading to a legislative deadlock where no progress is possible.

- If that scenario unfolds then Mr Trump would also face the same environment in reverse that Obama faced since 2008, except perhaps not to the same degree.

- Implications would include the potential for market volatility, which in turn harms confidence. We have already seen some market and exchange rate volatility in reaction to the election result. That might be short term, with early losses perhaps regained in part, but volatility may reappear each time Mr Trump and the House fail to align on a given issue.

Economic exposure:

- Mr Trump, departing from a traditional Republican position, supports maintaining the current level of spending for social programmes such as social security and raising the retirement age or benefit caps.

- Recently, Mr Trump has distanced himself from early statements about not increasing the minimum wage and he has made recent statements about increasing the minimum wage to $10 an hour.

- Mr Trump proposes significant tax cuts for individuals and corporations. He expects increased economic growth to offset the initial reduction in tax revenue.

- Mr Trump has proposed to increase spending by $550bn on national infrastructure and targets increased tax revenue from reduced restrictions on energy production to fund it (as opposed to increasing the gasoline tax).

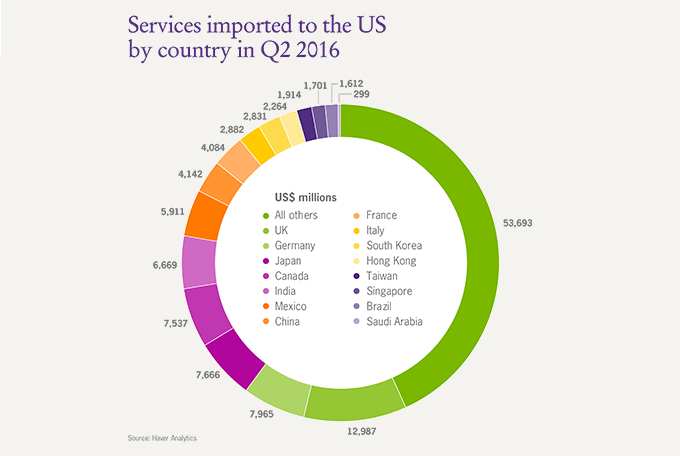

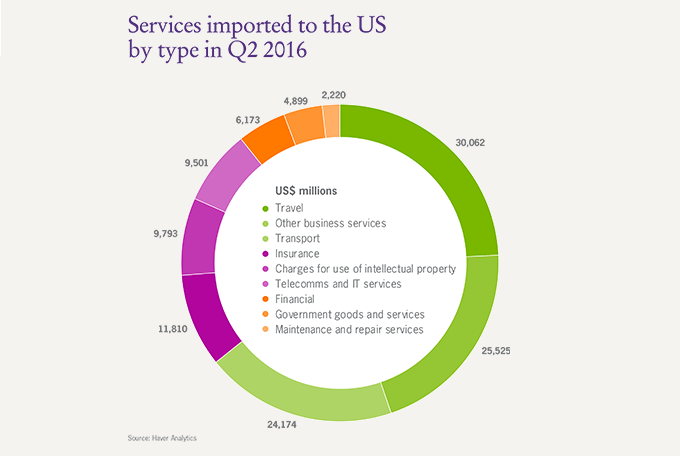

- The US is the world’s largest national economy with imports from all across the world; the following charts show, in US$ millions, those countries which benefit most from access to the US market and are therefore most exposed to related economic fluctuations:

![]()

![]()

Trade:

- Trade is an issue of conflict within the Republican Party. The traditional Republican Party represented business issues and was supportive of free trade. The new breed of Republicans – starting with the Tea Party movement in 2010 and representative of Mr Trump – is hostile to trade deals. He opposes the Trans-Pacific Partnership (TPP) and has spoken of pursuing a more protectionist agenda which could threaten for example the US’s commitment to the Transatlantic Trade and Investment Partnership under discussion with the European Union.

- More protectionist policies from the US mean that it will generally be tougher from an administrative perspective to export to the US, and more likely that the US will face retaliatory actions from other nations.

![]()

![]()

Markets:

- Mr Trump has on occasion given conflicting messages on issues like immigration, foreign policy and defence – the international markets may enter a period of volatility until his policies become clearer, and we know that volatility harms market confidence.

- Anti-trade measures imply that emerging market currencies will fall against the dollar, and emerging market shares/bonds would come under pressure. A stronger dollar makes exports to the US more competitive.

- That said, short term volatility in US markets means a weaker dollar which makes exports from the US more competitive, and exports to the US more expensive.

- Mr Trump said he’ll spend an additional $550bn on public infrastructure, which would imply an increased demand for emerging market raw materials.[1]

Interest rates:

- US interest rates are determined by the Federal Reserve and Mr Trump's statements on this topic have been conflicting. Lately, he has expressed support for Federal Reserve Chair Janet Yellen’s low interest policy.[2]

- The impact of electing Mr Trump on US interest rates is dependent on the policies he pursues. He has proposed massive tax cuts but no decrease in spending, which at face value would increase the public sector deficit and trigger an increase in interest rates. There is some question about the extent to which a Republican congress would allow this to happen – they might require more spending offsets than Mr Trump has previously entertained.

- US inflation is tipped to rise steadily if the oil price stabilises and US unemployment continues to fall thereby increasing consumer demand.

- Federal Reserve reaction to inflation rises is expected to be slow with steady increases in US interest rates.

- Protectionist trade policies could mean reduced price competition between US companies and as a result increased inflationary pressure. Or it could mean tariffs on imports which raises prices if imports in that sector are still bought by US customers. Or it could mean reduced inflationary pressure if a cheaper US product becomes the preferred purchase. Time will tell.

[1] www.bloomberg.com/politics/articles/2016-08-02/trump-says-he-ll-spend-more-than-half-trillion-dollars-on-infrastructure