IAS 36 - Recognising impairment losses

23 Mar 2022Step 6 of applying the guidance in IAS 36 as set out in our article ‘Insights into IAS 36 – Overview of the Standard’ and relates to recognising or reversing and impairment losses. This article focuses on part of this step; recognition of impairment losses. For reversing impairment losses refer to our article ‘Insights into IAS 36 – Reversing impairment losses’.

Step 6: Recognise or reverse any impairment loss

The requirements for recognising and measuring impairment losses differ based on the structure of the impairment testing as determined in Step 2 , discussed in our article ‘Insights into IAS 36 – Scope and structure of an impairment review’. The requirements for recognising and measuring impairment losses for an individual asset (other than goodwill) are addressed in firstly below; and then the requirements for recognising and measuring impairment losses for cash-generating units (CGUs) and goodwill are addressed after that.

Recognising an impairment loss for an individual asset

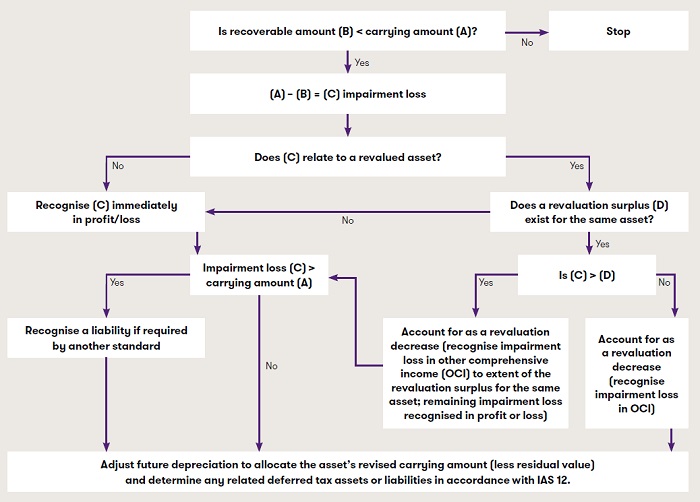

When the recoverable amount of an asset is less than its carrying amount, the carrying amount of the asset needs to be reduced to its recoverable amount and that reduction is recognised as an impairment loss.

For assets accounted for using the revaluation model in IAS 16 ‘Property, Plant and Equipment’ or IAS 38 ‘Intangible Assets’, the impairment loss is treated in the same way as a downward revaluation in accordance with those standards. Accordingly any impairment is recognised in other comprehensive income to the extent it does not exceed a previous revaluation surplus. Any excess is recognised in profit or loss.

To the extent the amount estimated for an impairment loss exceeds the carrying amount of the asset to which it relates, an entity shall recognise a liability if, and only if, required by another standard.

Practical insight – Impairment loss exceeds the carrying amount of the asset to which it relates

An unallocated impairment loss for an individual asset (ie a loss exceeding the carrying amount of the asset in question) might arise if the asset is expected to generate negative net future cash flows – for example an asset that is nearing the end of its economic life and requires significant decommissioning or holding costs.

In such cases the value in use (VIU) estimate would be negative. In addition, the entity might need to pay potential buyers to acquire the asset in which case fair value less cost of disposal (FVLCOD) would also be negative. In these cases, the entity would not reduce the carrying value of the asset to less than zero. The entity would look to IAS 37 ‘Provisions, Contingent Assets and Contingent Liabilities’ to determine whether a provision for decommissioning costs must be

recognised.

Finally, when an entity recognises an impairment loss for an individual asset, it must:

- adjust the future depreciation (amortisation) charge for the asset to allocate the asset’s revised carrying amount, less its residual value (if any) on a systematic basis over its remaining useful life (see example 1), and

- determine any related deferred tax assets or liabilities in accordance with IAS 12 ‘Income Taxes’ by comparing the revised carrying amount of the asset with its tax base (see example 2).

The below diagram summarises IAS 36’s requirements for recording an impairment for an individual asset.

Recognising an impairment loss for CGUs

An impairment loss must be recognised for a CGU when the recoverable amount of the unit is less than its carrying amount. IAS 36 prescribes the impairment loss to be allocated:

- first, to reduce the carrying amount of any goodwill allocated to the CGU

- then, to the other assets of the unit, pro rata on the basis of the carrying amount of each asset in the unit.

However, in allocating the impairment loss, an entity cannot reduce the carrying amount of an individual asset below the highest of:

- its FVLCOD (if measurable)

- its VIU (if determinable), and

- zero.

These amounts serve as a ‘floor’ as outlined in the below diagram.

If, for an individual asset within an impaired CGU, it is possible to measure FVLCOD but not VIU (and therefore not possible to determine the individual asset’s recoverable amount), then the floor is the higher of FVLCOD and zero. Under this scenario no impairment loss is recognised for the individual asset if the asset’s CGU is not impaired, even if the asset’s FVLCOD is less than its carrying amount.

Should the ‘floor’ be applicable for an asset; any amount that would have been allocated to the individual asset must be allocated pro rata to the other assets of the unit. The reductions in carrying amounts from applying the above requirements are treated as impairment losses on the individual assets and recognised.

The following diagram demonstrates allocating an impairment loss to assets within a CGU:

Download 'Recognising impairment losses' for an example that illustrates the interaction of these requirements in allocating the impairment loss to individual assets comprising a CGU.

How we can help

We hope you find the information in this article helpful in giving you some insight into IAS 36. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact or your local member firm.